Is this you? You have had a successful career and you feel like you have worked your tail off. As a result, you have always gotten over the obstacles that you have been presented with—at least so far. You know you are not an idiot, you’re a quick learner and you have succeeded almost every-time—at least so far. You are a student of the business and not only know the business but also how to effectively communicate the need along with that need’s respective solution. Whether your customers have been financial professionals or retail clients, those customers have always given you great reviews and as a result you produced—at least so far. You feel like it doesn’t matter what type of product or service you are given, you will always be able to use hard work and effort to make sure that you succeed—at least so far. Do you love your work, your quality of work and take pride in doing a good job as well as getting well compensated for it? Is this you?

Is this also you? As much fun as you have had over your career and as much money as you may have made, you have begun to feel somewhat of a sense of emptiness. Is this emptiness brought about by the feeling that you are not able to influence your business as much as you would like because, in short, you work for somebody else? Furthermore, do you feel that, because you work for somebody else, the ideas that you would like to run with—that you know from your vast experience will work—are not being implemented? Do you feel that there is an imbalance between how much you care about your job and how much your job cares about you? Is this you?

Now, is this also you? Have you occasionally thought to yourself, “Then why don’t I start my own IMO/GA/agency?” But every time you ask that question, does the devil in your ear say that you will fail? That devil in your ear says, “Yes, you have been successful, at least so far, at almost everything you have done—but this time is different. Starting a business is different and you will fail.” That devil in your ear has also said things like the below:

- “The amount of knowledge around technology that you need today is beyond you…after all, you are a salesperson!”

- “You don’t have enough contacts to get the business running quickly.”

- “The IMO/GA/agency business is consolidating and only the big ones will succeed.”

- “You need massive contracts in order to succeed, which are very hard to get at the outset.”

- “Staffing at the appropriate levels is astronomically expensive.”

- etc.

- etc.

- etc.

If you are somebody currently in the position that I just explained, or one of the many successful IMO/GA/agency owners that read this publication, you are probably nodding your head because you know what I am talking about. You are either there, or you have been there.

The purpose of this article is to explain my high-level observations since I started my own marketing organization months ago, after several years of listening to the devil in my ear and not doing so. If I can help somebody change their lives for the better by writing about my experience then it was worth it. Much of the fine details are beyond the scope of this article, so if you want further advice please contact me.

Just Do It

I remember as a kid seeing old western movies where the cowboy would pull up to saloon on his horse, get off the horse and take the leather “leash” and merely wrap it one time around the post in order to keep the horse from bailing while the cowboy went to drink. As a kid, I always wondered how that would keep the horse in place. Heck, if the horse pulled just a little bit instead of just standing there, he/she would realize that it can run free! That is the equivalent of the devil in our ear. That devil is the psychological “leash” that tells us to just stand there and not pull.

Your gut is almost always more accurate than the devil in your ear. If you feel in your gut that you are the person I described in the first few paragraphs, and if you are financially able to—then rip the leash from the post! The other concerns about your ability to handle the technology, etc. will take care of themselves once you jump in. That’s right. Jump in and figure out the minor details later! If you have a value proposition and a plan/strategy for getting that value proposition in front of the right people, don’t sweat the small stuff yet.

One year ago I never would have thought that I could create a website, an agent microsite, marketing material, or a company “network” in our office. I was wrong! This stuff is not that hard! Although I am getting to a point where I don’t have time to do all the minor stuff and am hiring for it or outsourcing it, I learned that I am much more capable than the devil in the ear told me I was. You would be the same if you are the person in the first few paragraphs.

Again, if you have a value proposition that is unique from your competitors, don’t worry about what the “bigger guys” are doing. We have all read about the success stories of companies like Microsoft, Apple and Walt Disney, and how they started their businesses when the odds were stacked against them. But they succeeded! If you have a unique and strong value proposition relative to your competitors you will succeed.

But first, a word of caution about money—because that is one of the top determinants, if not the top, of whether you are able to do this.

You Need Money To Make Money

Now the bad news. There is truth to the cliché of “needing money to make money.” While starting an agency is not like starting a construction business, where you might need several pieces of $500,000 machinery, you still need money. Your LLC can be started with merely a couple hundred dollars. However, there are many other expenses—most of them technology. Here is a list off the top of my head: Errors and Omissions (both personal and agency), state insurance licensing fees for each state, computers, printers, website provider, antivirus/firewall for your network, email service like Constant Contact, Gotowebinar/WebEx, prospect lists, agency management system, health insurance. And the last one: Ultimately, if your business starts taking off, you will need staff!

Two additional thoughts about “needing money to make money” are:

- I believe that, whether one is a principal of an IMO or just a personal producer, with today’s regulatory environment he/she should have an affiliation with a broker/dealer or an RIA firm—especially the RIA firm. The fiduciary genie is out of the bottle, if not from a regulatory standpoint then certainly from a client mentality standpoint. I have been asked a few times by some personal clients if I was a “fiduciary.” Now you are probably like me in that you always act in the clients’ best interest whether you are officially a “fiduciary” or not. However, licenses matter to the regulators! One of the first things I did when I started my business was to retake my Series 66 and Series 7 exams (I dropped them years ago). Not only did the exams cost money, but the fees associated with the BDs/RIAs range anywhere from $1,000 per year to upwards of $7,000 per year. I believe that in order to build a healthy business in financial services and to hedge against regulatory uncertainty you need a securities license. Starting your own business is an opportunity to start a business the healthy way.

- The main reason I believe you need a large cushion before you start your own IMO/GA is because of this: Relationships with agents are just like relationships with consumers. It takes time to develop. Before I elaborate, let me step back a second and discuss my opinion on the genesis of the negative reputation that “insurance agents” have. I think one of the reasons our profession has gotten the reputation it has is rooted in the way that many of us got started in the business. I was almost straight out of college when I worked as an agent for one of the big career insurance companies. I was on a “commission draw” that the company gave me for the first six months, which was good because I had virtually no money because I was young. On the very first day of my employment the clock started ticking for me to produce so I could offset that “draw” with commission. If this didn’t happen, I would be gone six months later. The urgency was huge. On day one I knew nothing about the business, but I did know the phone numbers of my friends, relatives, and even a few people I hadn’t spoken to in ten years that I was sure would be thrilled to get a call from me (sarcasm). Needless to say, over that first year I was more “aggressive” with potential customers than I am today. Why? Because I needed to be. I needed to put food on the table! I had no cash cushion.

The fact that I have been smart with my money over the years allows me to follow the pace of the customer, whether those customers are the agents or my personal clients. I am not going to starve if an agent does not have an immediate need for my services. Persistence and patience always win! Money buys patience and patience earns trust. Trust is what our industry revolves around.

Buy It As You Need It

Although you need money to make money, the good news is that you don’t have to go crazy at the outset. One thing I learned about running my own firm is that you get solicited every day. Everybody is calling you offering you this system or that system. It would eat up your whole day if you allowed it to. And some of the systems are good and you get tempted to buy. But at the outset there are certain things that you do not need, at least not until the proper time comes. For instance, one of the first systems I bought was Gotowebinar. Webinar was obviously crucial because this was how I was going to discuss my value proposition with my potential customers/agents. This was needed at the outset! On the other hand, I did not need to buy licenses in all 50 states at the outset so I didn’t. Now, however, every week I am buying a new license for a new state as a new agent from that state submits a case. Let the revenue precede the expenditures whenever possible! In other words, it’s easy to justify spending $100 to get licensed in XYZ state when there will soon be a $1,000 override check coming because of it.

So Many Reasons To Do It

- As mentioned, if you are who I described in the first few paragraphs, then building your own business is for you. Here are just a few reasons that you should run your own company:

- When you run your own business, it is very satisfying to know that every minute you work, every idea or tool that you create, is going toward the value of your company.

- You are building a legacy for your family, should they ever want to work with you.

- When you run your own company you can do business with whomever you wish. In order to run a healthy business you need to do business with those that will not be a liability to the firm—whether literally or figuratively. I have had to tell a handful of folks that I would not pursue a partnership with them for this reason.

- The upside is unlimited. I have a friend that just sold his IMO for a very large sum. I was talking to him about money. I said, “How long did it take you to make merely six-figures when you started your own IMO?” He said, “Five years.” I was hoping he would say five months! However, he then came back and said, “But I made seven-figures within ten-years and this was 30 years ago.” That is real money. Again, if you have the cash cushion and the time, it will be worth it.

Final Tip

I have been in the industry for over 20 years, have worked with many BGAs/IMOs and have learned what to do and what not to do. I have seen some awesome firms that have created their own awesome empires. I have also seen firms that have been built in an “unhealthy” manner. However, they have gotten so big that they can’t change now. In your company’s infancy, you have the opportunity to kill that monster while it is still a baby. Kill those bad habits and inefficiencies before they grow! (I wish somebody showed me the correct golf swing when I got started 20 years ago!)

Build your company the right way from the beginning by having a securities/fiduciary affiliation. Build your company the right way by being patient with your customers versus high pressure overpromise/underdeliver tactics. Build your company the right way by focusing on the relationships versus the transactions. When people do business with CG Financial Group, they do business with me personally, not the company. Don’t lose sight of that! I have seen many companies get big and have the founder get too “disconnected.” Thus, the culture that attracted customers/agents to the firm is now gone.

Lastly, build your company the right way by affiliating with other IMOs/agencies that will give you great advice. I have learned that when you go out on your own, you realize who your true friends are—those who truly want you to succeed versus those that view others’ success as a zero-sum game. As it turns out, I have many friends that have given me a lot of help. You know who you are, and I will forever be grateful.

")

What I Learned From The Time I Thought I Was Going To Die

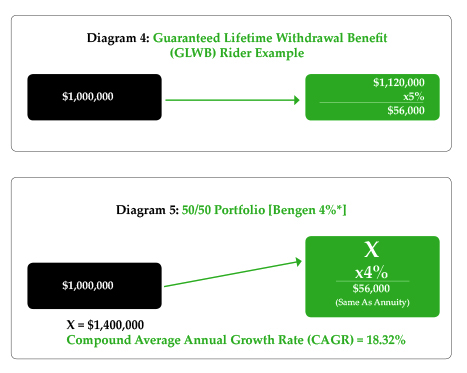

On March 9 we passed the ten-year anniversary of the bull market that started in 2009; almost tripling the duration of the average bull market. Since March 9, 2009, the S&P 500 has quadrupled. Now, by just looking at the duration of the bull market and comparing it to past bull market lifespans, that would be a rather simplistic approach to arriving at a prognostication of what the future holds in the market. Although my intent is not to “prognosticate” anything in this article, I have my opinions and will say that the more “analytical” approaches to coming to a prognostication would indicate that we could be in for a rough ride. I research the market a lot and I believe that more can be found in the behavior of the bond market than the stock market. Without going into a long description, I will say that inverted yield curve is not good! An inverted yield curve has preceded every recession in the last 60 years.

As we face the possibility of being confronted with significant angst from our customers, I thought it would make sense to repeat a message from one of my Broker World articles from a couple of years ago as I believe it warrants repeating.

About ten years ago I had a 6:00 am Southwest flight out of Omaha to Phoenix. I was dead tired because I had to wake up at 3:30 am to get on the flight. Nevertheless, I dragged myself to the airport. Waiting at the gate to get on the airplane seemed to take forever. All I wanted to do was get on the plane and take a nap. As I boarded the plane I was happy because there were probably about 50 people on the flight which would mean that I would likely have plenty of room to get comfortable and take my nap. Indeed, after I sat down I noticed that in my row it was just me and somebody across the aisle in the other seat that looked like he was probably a frequent traveler, as am I. Without going into detail, this guy looked the part. Anyway, as I sat there in my seat I started to doze off into a half-conscious state. I could feel the plane pull back from the gate and go through the long process of idling out to the runway. The feeling of the plane lumbering along through the obstacles to get to the runway is kind of a soothing feeling, a lot like rocking a baby to sleep. In my half-awake state I could then feel the plane’s full thrust kick in as I was pushed back in my seat. It was obvious we were now making our way down the runway. As we made it down the runway we were nearing the final stage where you just begin to feel the front wheel lift as we go airborne. Then, suddenly, BOOM! This is the point when my whole world got rocked. It felt like we hit a brick wall as I was jolted wide awake. We were then skidding down the runway as I pulled myself to the window in panic to see where the end of the runway was because we had to be close. I also glanced over at Mr. Frequent Traveler across the aisle, whose eyes were the size of dinner plates. He was looking back at me for confirmation we were not going to die, which I could not provide him. He was panicking, the other passengers were panicking and, worse of all, the flight attendants were panicking! By the way, when the flight attendants panic, you should panic too!

What felt like a lifetime finally came to an end. We finally slowed down and got it under control. As the dust settled and we began that slow idle back to the gate I could hear people sobbing toward the back of the plane. That is when the captain came on the intercom to tell us what had just happened. What did he say? In a very calm and stoic voice he comes on and says “Hello folks, sorry about that somewhat uncomfortable take-off attempt. As we began to get airborne we had a diagnostic code tripped in the system that indicated the right-side engine was failing so we had to abort our take off. We will have to take you back to our gate and see what we need to do to get you on your way home. We do apologize for the inconvenience and greatly appreciate your patience as we get you home safe and sound.”

With those calm words from the pilot, suddenly everything seemed OK! You would have thought that the pilot had been there and done that a million times! Isn’t it amazing how a few calming words can put you at ease? I had flown hundreds of flights a year up to that point and I knew that this incident was not normal for me nor for anybody else, including the pilot! I knew that flight was a near death experience. I knew this, my friend across the aisle knew this, and the flight attendants knew this. Even more interesting is, even though I also knew that it was the pilot’s job to project a sense of calm even if he were to think we were all going to die, it still worked! A lot like when you tell yourself a salesman is going to try to sell you something and you aren’t going to buy it. But once you hear the pitch you buy it hook, line, and sinker.

The calm reassuring voice of the pilot put me and everybody else at ease even though I knew it was his job to create a false sense of security. The pilot became an instant hero. As a matter of fact, as we were deplaning I noticed several people hugging the pilot as they walked past.

When we got into the gate I called my friend who worked for another airline who pulled the incident up in his system. He said that incident I had just gone through was indeed a very big deal. He said that the airplane had been so far into the takeoff process that it passed what is called “V1” which is basically the speed of no return. He had stated that for the pilot to make the call to abort the takeoff at that point was a tough call because it was a choice between either getting airborne and having the plane fail in the air or aborting and running out of runway and crashing on the ground. The pilot chose option number two and fortunately it turned out fine.

My point is, you are your clients’ airplane captain. When they call you up because they are hitting turbulence in their lives, whether because they are losing money in the market, have a death claim, a long term care claim, etc., your value in these times lies in the way that you handle the situation. This is your opportunity to become a hero by doing the opposite of panicking and instead being a steady hand to those that are panicking. This is what top financial professionals do. They project a sense of “I have been there and done that and we will remedy this situation.” Imagine instead if that pilot came on the intercom and screamed out “Take cover! We are all going to die!” Panic is contagious and so is calmness. And people remember the “heroes” that gave them calmness in times of distress.

Are you that calming voice even at times when you are also scared for the client?

When I was getting started in the business there were times where I would get “panicky” because of a big meeting I had to conduct, a bad message I had to give to somebody, or a large audience I had to present to. I had a mentor back then who would always say, “You have done this a million times, and have you failed yet? No, you haven’t! So why panic now?” He would then go on to say “So what is the worst that can happen if you were to fail? It’s not like they can kill you.” For some strange reason those words have always stuck with me, “It’s not like they can kill me.”

We take our business very serious but keeping a perspective of what is important in life will also help you to not panic when things get stressful. We tend to let the negative trash in our heads believe that it’s a life or death situation if we fail at a task. It is not. This is why I have the utmost respect for our courageous men and women in the military. Their bad days on the job are way beyond the average person’s.

Not panicking is not only healthy for you, it is also healthy for your clients and your relationship with those clients. This is because having a positive mindset is a self-fulfilling prophecy. Meaning if you are always positive and never panic, clients feel that and will, in turn, be positive and will not panic. You are looked at as the “pilot” and therefore the creation of a positive environment is in your hands. Prospects/clients look to your mindset to form their own. And, the mindset that you have over the coming years could be extremely important if the market does what it is overdue to do.

Also remember, in almost any study out there that asks consumers why they left their advisor, the top response is almost always about communication or lack thereof. When the going gets tough, the tough communicate with their clients.